September 12, 2025

10 min

The Hidden Cost of Broken Q2C — and How AI Actually Fixes It

Introduction

Quote-to-Cash: Why It’s a Minefield, Not a Pipeline

Beneath every B2B sales engine runs the “quote-to-cash” process — a chain of fragile hand-offs where cash leaks, margins erode, and customers disappear without a word. It’s not a neat pipeline. It's an operational quicksand, and most P&Ls hide the true scale until it’s too late.

Ask yourself: Are you losing cash because quotes are slow, discounts sprawl, invoices bounce, or credit checks stall good orders? These are hidden drains on working capital and reputation. And almost every system in the Q2C chain can break in ways that quietly punish both cash flow and customer trust.

Why AI Can Close the Gaps (But Only with Real Control)

Many executives see AI as the answer, but the era of pilots and hype cycles is over. Regulators (especially in Europe) now expect provable control — actual evidence that AI usage is governed, transparent, and accountable.

EU AI Act Timeline:

- Feb 2, 2025: Ban on prohibited uses; minimum AI literacy requirements.

- Aug 2, 2025: Obligations for General-Purpose AI kick in.

- Aug 2, 2026: Most high-risk requirements become law.

- Aug 2, 2027: Embedded high-risk AI requirements in regulated products go live.

- Penalties reach €35m or 7% global turnover for prohibited practices.

If your Q2C leverages AI for decisioning or customer contact, you now need documented oversight — not just a good story.

What’s Actually Leaking (and How You Spot It)

Look beneath the surface of your P&L and you’ll find key metrics slipping:

- Days Sales Outstanding (DSO): Every extra day locks up cash you’re financing at 7–9%.

- Revenue leakage: Unenforced terms and sloppy discounts quietly shave 0.5–2.5 percentage points — often missed in complex contracts.

- Disputes & rework: Failure to get orders/invoices right the first time jams collections downstream.

- Credit holds: Static limits and stale signals stall well-meaning orders while missing real risk.

- Manual grind: Orders entered from emails and PDFs, remittances keyed by hand, generic collections.

- E-invoicing & tax rejects: Each rejection delays cash.

- Customer experience decay: Opaque collections, slow responses, missing Proof of Delivery — customers leave silently.

- Regulatory exposure: Use AI in credit or collections? You now face oversight on lifecycle risk, transparency, and governance.

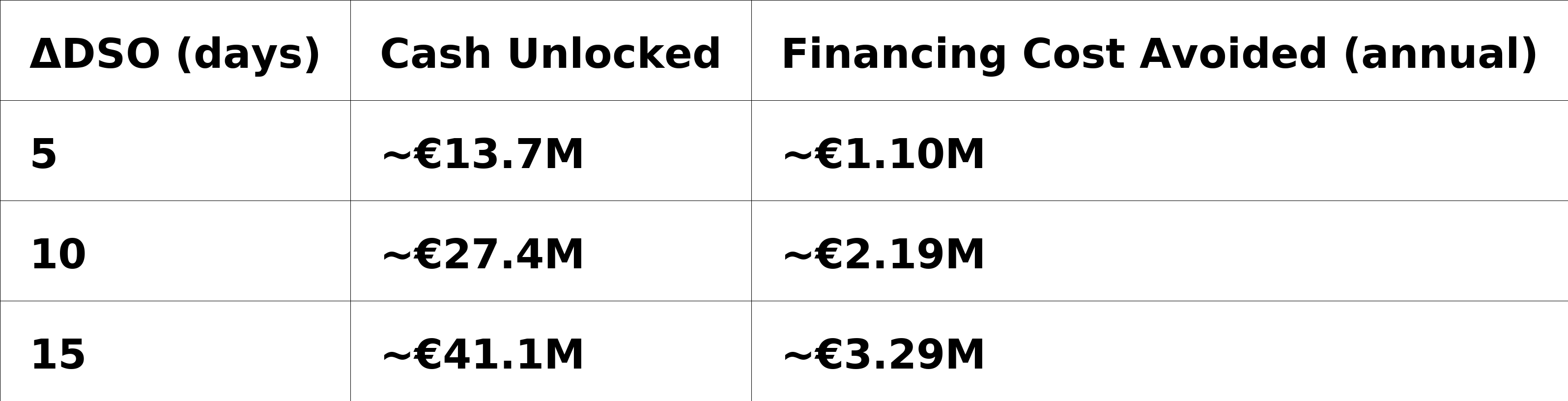

Napkin Math: €1B Business Example

Use these one-line formulas:

- Daily Net Sales = Annual Revenue ÷ 365

- Cash Unlocked = Daily Net Sales × ΔDSO

- Financing Cost Avoided = Cash Unlocked × Cost of Capital

Other levers:

- Lower leakage by 1pp = ~€10M high-margin protected revenue.

- Smarter contact strategy & voice automation = multi-million run-rate savings if you build in disclosure and human-in-the-loop integration.

- Bad debt down 0.2pp = ~€2M per year.

Where AI Delivers (If Governed, Measured, and Embedded)

Here’s how AI fixes each weak link in Q2C, with the artifacts to prove control:

1. Quote & Pricing

- Symptom: Slow quotes, unmanaged discounts.

- AI: Config assist, discount guardrails, clause assembly.

- KPI: Lead time −30–70%, margin discipline +1–2pp.

- Artifact: Pricing model card, override logs, explainability notes.

2. Contracting

- Symptom: Terms misaligned with billing/fulfillment.

- AI: Clause extraction, deviation alerts.

- KPI: Fewer disputes, faster invoice acceptance.

- Artifact: Deviation register, indexation checks.

3. Order Management

- Symptom: Chaos from email/EDI, wrong SKUs.

- AI: Unstructured intake, validation, exception routing.

- KPI: First‑time‑right rate ↑, disputes ↓.

- Artifact: Intake trace, auto-validation logs.

4. Billing & E‑Invoicing

- Symptom: Rejections, ID errors.

- AI: Pre-validation, auto-correction.

- KPI: Lower reject rate, faster acceptance.

- Artifact: Validation reports per jurisdiction.

5. Cash Application

- Symptom: Unapplied cash, dirty remittances.

- AI: OCR & parsing, ML matching.

- KPI: 80–95% auto-match, unapplied cash ↓.

- Artifact: Match rate by payer, aging reports.

6. Collections

- Symptom: Generic dunning, poor promise-to-pay.

- AI: Risk-based prioritization, bots, auto notes.

- KPI: Average days delinquent ↓, contact effectiveness ↑.

- Non-negotiable: Disclose AI use, log interventions.

- Artifact: Disclosure scripts, HITL intervention logs.

7. Disputes & Deductions

- Symptom: Long cycles, high write-offs.

- AI: Root cause classification, evidence packs.

- KPI: Shorter cycle, fewer credits.

- Artifact: Taxonomy drift report, disposition codes linked to credits.

8. Revenue Assurance

- Symptom: Indexation/rebate leaks.

- AI: Contract-to-invoice checks, index enforcement.

- KPI: Leakage −0.5–1.5pp.

- Artifact: Enforcement trail, rebate reconciliation.

Who Owns Q2C AI? The Triad Model Wins

IT, Operations, Finance: Don’t pick just one department.

- One executive (usually P&L owner) is accountable for outcomes.

- CAIO co‑owns governance (with veto).

- IT and Operations jointly build and run tools, sharing KPIs.

This triad model ensures AI crosses from “pilot” to operational control — backed by real outcomes.

Governance: Built In, Not Bolted On

Endpoint controls aren’t enough. Governance must be part of Q2C’s design:

- ISO/IEC 42001: Your system for AI risk, roles, oversight.

- NIST AI RMF: Practical, auditable risk playbook.

- GPAI Code of Practice: Transparency and safety until harmonized standards arrive.

Act Now: Bans and literacy (Feb 2025). GPAI duties (Aug 2025). Most high-risk obligations (Aug 2026). Embedded high-risk (Aug 2027). The compliance timer is ticking for every multinational.

Ten Controls to Stand Up in 90 Days

- Inventory all models/agents with named owners.

- Use-case intake gates (purpose, data, red flags, go/no-go).

- Artificial Intelligence Assessment (AIA) + Privacy Impact Assessment (PIA) at intake and pre-production.

- Third-party diligence (provenance, IP, model cards).

- Red-teaming (prompt-injection, leakage, harmful output).

- Human-in-the-loop interventions, logged with SLAs.

- Monitoring and immutable logs (drift, fairness).

- Change control (prompt/versioning).

- Disclosure patterns for human/AI interactions.

- Training and annual attestation for all operators.

KPIs That Prove Real Value

- Cash & risk: DSO, ADD, % overdue, bad debt rate.

- Quality: First-time-right, dispute cycle, reject rate.

- Collections: PTP kept, cost per touch.

- Cash App: Auto-match rates, unapplied cash.

- Revenue assurance: Leakage, indexation compliance.

- Governance: % high-risk/GPAI with assessments, model cards, workforce training.

Avoiding Common Pitfalls

- Ethics theatre: Attractive slides, no process controls. Fix: Embed gates and logs in workflow.

- Tool worship: Great demo, poor adoption. Fix: Prioritize integration and user fit.

- Blind spots with third parties: No documentation, no incident protocol. Fix: Diligence in procurement.

- Change-management failure: Frontlines left out. Fix: Train and attest, annually.

Practical Steps You Can Take This Quarter

- Gap-assess controls against ISO/IEC 42001 and NIST AI RMF.

- Appoint a Responsible-AI lead with board-level support.

- Stand up the 10 controls. Begin logging every decision.

- Align contracts and supplier obligations to EU AI Act milestones (GPAI rules are active this August).

- Prioritize fast-ROI moves (cash app, smart collections, invoice validation) and design for integration, not just demo.

Case Note: How Governance Changes the Result

A multinational with escalating overdue and unapplied cash started with two controls—invoice pre-validation and risk-based collection calls. Under a single P&L owner, the Finance, IT, and Operations triad embedded disclosure and human-in-the-loop logging. Within a quarter, rejection rates plummeted, ADD improved, and manual work dropped. Governance wasn’t a barrier—it made scale and auditability real.

FAQs

Can we skip governance until we scale?

No. Regulatory timelines are live, controls are cheap to start and expensive to retrofit.

Who “owns” Q2C AI?

Run the triad, with one executive holding outcomes. Shared KPIs beat siloed projects.

What if our data isn’t perfect?

Prioritize the biggest loss areas. Instrument controls as you automate. Pick tools for scale, not just sizzle.

How do we show progress to the board?

Use the KPI set above: cash, quality, collections, governance coverage. If those move, transformation is real.

Final Thought

If your initiative isn’t delivering on cash conversion, stopping margin leaks, or crushing operational cost, it’s just AI theatre. The difference is governed AI, triad-owned Q2C, and hard KPIs—turning “innovation” into audit-proof cash-flow you can defend in any boardroom.

.png)

.jpeg)